Voting Resources

What Should Happen with the Joe Corley Jail?

Is the sale of the jail, which the County will continue to lease, the best way to resolve the problems the County has created by building a jail which the County does not currently need?

Is the sale of the jail, which the County will continue to lease, the best way to resolve the problems the County has created by building a jail which the County does not currently need?

Texas law allows Counties to issue Revenue Bonds, which are secured by the revenues of a project, without voter approval. But it is inconceivable that the legislature intended this provision to be used where the source of the revenue is not a third party. That is exactly the situation created by the Joe Corley Jail financing. The County established a special purpose company and then made itself the source of the revenue to repay the bonds. While this arrangement may have met the letter of the law, it is unimaginable that it met the spirit of the law. The members of the Commissioners’ Court who participated in this deception should be ashamed of themselves. It appears that the only conceivable reason this financing was structure this way was to avoid having to ask voters to approve the County using their credit for a deal like this. And that is outrageous.

Which raises the second point. Did any of the members of the Commissioners’ Court campaign on the basis of their entrepreneurial and creative financing skills? No, none of the politicians who voted for this deal were elected for this purpose. And the mess we have with the Joe Corley financing is exhibit number 1 as to why taxpayers do not want their elected officials expanding government into areas where we are on the hook for commercial risks. So far, what has happened to the Joe Corley financing is due to the County making a commitment on the jail’s utilization that made no sense. But the commercial risk continues, since there is no way anyone knows whether the federal use of the facility, which is committed only for 100 day increments, will continue. And if it doesn’t, does anyone really believe the County will risk its credit rating by not continuing to appropriate the lease payments?

Joe Corley is a classic example of what happens when government gets into activities it shouldn’t. This expansion of government is a liberal action taken by people on the Montgomery Commissioners’ Court who claim to be conservative. This is not an example of limited government; it’s an example of expansive government. It is also, sadly, appears to be an example of not only a total lack of transparency, but possibly an intentional effort to dupe and bypass the voters. It is an example of why the Tea Party exists and why it is so important. We the people have negligently assumed our elected officials would behave responsibly. This appears to have been extremely naïve.

Finally, there is the question of how involved voters should be in their government committing them to debt. Joe Corley may be the second example in the last 12 months of Montgomery County Commissioners’ Court intentionally trying to bypass the voters when committing to debt. The first example was the use of Certificate of Obligation to bypass (at least in part) the will of the voters when they refused to approve the County’s bond referendum in November, 2011. During 2012, the County issued two $15 million Certificates of Obligation, at least part of which appeared to fund projects that the voters turned down in the 2011 referendum. Due in part to lobbying by the Texas Patriots PAC, Senator Tommy Williams introduced earlier this year legislation that somewhat restricts this kind of activity. And we will be pushing for more restrictions. The one good thing about the Joe Corley Jail financing is that it provides a terrific example of why the County should be required to seek voter approval of all borrowings except in the case of an emergency. Forcing the County to justify most of their borrowing should increase transparency and help eliminate Joe Corley type disasters in the future.

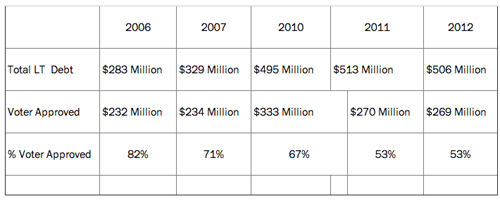

To reinforce the position that the County has increasingly bypassed voters’ approval for debt, the following chart shows how since 2006, the percentage of Montgomery County long-term debt outstanding approved by the voters had fallen from 82% to 53% as of September 30, 2012. The actual percentage today may be even lower since the 2012 number does not include the second $15 million Certificate of Obligation issued by the County in calendar year 2012.

Background

The new County jail facility was first mentioned the 2007 Montgomery County Annual Financial Report. In a section in titled “Long-term financial planning” the report stated the following:

Recognizing the immediate as well as future need for more bed space in the county jail, Commissioners' Court created the Jail Financing Corporation … to raise the funds necessary to construct an 1,100-bed detention facility adjacent to the existing jail. The Corporation issued $45million in lease-revenue bonds during 2007, and construction is currently underway. Upon completion, the facility will be leased to the County by the Corporation to initially house federal inmates under the terms of an intergovernmental agreement … with the federal government. Revenues received from housing the federal inmates will, in turn, be used to retire the outstanding bonds. The County anticipates "opening up" an estimated 250 beds in the existing jail by transferring current federal inmates to the new facility.

A later section in the 2007 Report stated: “The County issues three types of debt; general obligation bonds are approved by the voters of the County while lease-revenue bonds and certificates of obligation are approved by Commissioners’ Court. ...The lease-revenue bonds are secured by a pledge of future revenues to be earned under an agreement between the County and the Montgomery County Jail Financing Corporation.” A similar statement has appeared in each Annual Financial Report since 2007.

One important fact the County did not disclose until late last year was that to minimize the cost of the bonds issued by the Jail Financing Corporation, the County obtained a ruling from the IRS designating the interest paid on the bonds as free of federal income tax. In its ruling request, the County represented that by August, 2013 at least 30% of the inmates in the new jail would be County prisoners. The ruling was based on this occurring. However, this will not happen. The County has never had its prisoners at the new facility due to a combination of: 1) freeing up the 250 beds with the transfer of federal inmates to the new jail; 2) the remodeling of the old jail to accommodate 300 additional prisoners; and 3) lower than expected growth in the number of County prisoners. As a result, the County expects the tax free status of the jail bonds to be lost when the IRS becomes aware that the County is not utilizing the new jail. The Commissioners’ solution to this problem is to sell the jail! The Commissioners’ have refused to consider other options, like refinancing or renegotiation with the current bondholders, which would retain the County’s ownership of the facility.

Reporting Issues

The County’s 2007 Annual Financial Report described the jail financing in two contradictory ways. First it stated that the revenues from the intergovernmental agreement would be used to fund the repayment of the jail bonds. Then it said that the lease payments by the County to the Jail Financing Corporation would be the source of the bond repayment. Which one is it?

Based on documents made available to us through an information request to the County, the answer is the lease payments by the County are the only source of the revenue the bondholders are looking to for repayment of the debt. In fact, the bonds issued by the Jail Financing Corporation make no mention of the federal payments. And the County’s lease payments are due at the same time and in the exact amount of the Jail Financing Corporation’s payments on the bonds. The County hopes that the revenues from the federal use of the jail will be sufficient to fund both the cost of operating the jail and the debt service on the bonds. But there is no certainty this will happen; this is a gamble the County has taken on the taxpayers’ behalf.

The County’s obligation to make lease payments is subject to the appropriation of the lease payments in each annual County budget. Under the terms of the Lease, the County is obliged to submit the lease payments each year for appropriation. But the County is not required appropriate funds for the lease payments. However, the County cannot assume receipt of federal revenue from the jail as the source of funding for the lease payment appropriation because the federal intergovernmental agreements are only for 100 days, and, therefore, are not a secure revenue source for the entire budget year. So in appropriating the lease payments each year, the County has to either use general revenue funds or take the risk that the intergovernmental agreements will continue to pay sufficient funds during the year to fund the lease payments. If the County is taking a risk, what happens if the federal payments are insufficient? Is this a prudent way to run the government?

So why did the 2007 Annual Financial Report state that: “Revenues received from housing the federal inmates will, in turn, be used to retire the outstanding bonds”? I’m not sure about the answer to this question. But I wonder: could this be to an attempt to bolster the County’s claim that the bonds issued to fund the jail are lease-revenue bonds; a category of bonds that do not require voter approval because they are self-liquidating and not backed by the full faith and credit of the County?

What drives me to wonder whether this is what is going on is that some members of the Commissioners’ Court have portrayed the jail financing as a “project financing”. “Project financing” is where the lenders fund a project based on the project’s assets plus a stream of payments that are due from a third party under a long-term contract which is to be performed by the project. Applying the term “project financing” to the Joe Corley Jail financing, however, is at best a misnomer. It would require treating the County as a third party to the Jail Financing Corporation, which is ridiculous. The County created and wholly owns the Jail Financing Corporation, the Board of Directors of the Financing Corporation are the members of the Commissioners’ Court, to the best of my knowledge the Financing Corporation has no employees and the County consolidates the jail’s bonds on its balance sheet. The only fact pattern that would make the Joe Corley Jail financing a “Project Financing” is if “Revenues received from housing the federal inmates” were pursuant to a long term contract and the bondholders were looking only to the revenues from that contract “to retire the outstanding bonds.” But the reality is that this is not the case; the bondholders are looking only to the County’s lease payments and the jail asset, for repayment. The feds are not part of the picture from the bondholders’ point of view.

Some of the Commissioners have also maintained that the jail financing is “nonrecourse” to the County. “Nonrecourse” is a central feature of “project financing” and allows the project owner to walk from both the project and the project’s debt obligation and the lender cannot go after the owner for repayment. The project owner of the Joe Corley Jail is the Jail Financing Corporation. And since the only asset of the Jail Financing Corporation is the jail, nonrecourse is somewhat meaningless. But nonrecourse to the County, which is the source of the revenue to repay the bonds, is important. And technically the bond agreement makes it clear that the bondholders cannot look to the County for repayment if the County decides not to appropriate funds to pay for the lease, making the financing nonrecourse to the County. But this may be a smoke and mirrors situation. Failure by the County to appropriate the lease payments is not a default by the County under the lease, but it is a default by the Jail Financing Corporation under the terms of the bonds, and would: 1) trigger the bondholders taking ownership of the jail (a jail that at the time the bonds were issued, the County claimed it needed and would be using 30% of by 2013); and 2) result in a likely downgrade in the County’s bond rating because the County willfully created a default by an wholly owned subsidiary company. So, while the bondholders explicitly recognized the County’s right not to appropriate the lease payments, they judged the cost to the County of not doing so as so severe that the lease payments would always be appropriated. And I suspect they were probably correct.

Sale of Jail Issues

It is incomprehensible how the County could have expected to utilize 30% of the new jail while expanding the size of its existing jail by approximately 550 beds. So with hindsight (which is always 20/20), one would think that the tax problem facing the jail bonds today should have been anticipated by the Commissioners’ Court, or at least by their expensive advisers, from the onset. But obviously, had that been the case, the Jail Financing Corporation would never have issued tax free bonds in the first place. The Commissioners owe the public an explanation on how this miscalculation arose, especially since this miscalculation will likely cost the County (and, by extension, we taxpayers) money. And the people responsible for this error should be held accountable.

But it is equally incomprehensible why the Commissioners’ Court is selling this asset without first taking the time to study and evaluate other options. At the time the decision to sell the jail was made, James Noack, who was the Precinct 3 Commissioner elect, urged the Court to do this kind of evaluation before making a decision, but was ignored. Here are the facts.

The request for proposals to buy the jail states that the sale is subject to the lease between the County and the Jail Financing Corporation. In other words, after the sale of the jail, the County will continue to make the lease payments due under the lease, which continue until 2028 and total more than $38 million plus interest! For this the County expects to get enough from the sale of the jail (the minimum price has been set at $55 million) to repay the existing bondholders (approximately $45 million) and leave the County with a $10 million profit. But once the jail has been sold, at the end of the lease the County will not own the jail. Wasn’t the acquisition of this jail facility the reason the County entered into this Joe Corley transaction to begin with? And, if by then we are housing County prisoners in the jail, we will either have to renew the lease for use of the jail, buy the jail at its then fair market value or build a new one. On top of all this, the County has already paid almost $7 million plus interest on the jail bonds.

So let’s see. The County has already paid $7 million plus interest for the jail, expects to net a $10 million “profit” from the sale of the jail and then will pay $38 million plus interest to lease the jail for the next 15 years. At that point, the jail will be owned by whoever buys it and if the county needs more jail space, it will either have to enter into a new lease for the jail, buy the jail or build a new jail. The County will continue to take the risk that the federal government payments are sufficient to cover the cost of operating the jail plus the cost of the lease payments. And we are expected to accept this as a good deal? The Commissioners’ Court has to justify why this is the best solution to the problem the County has created for itself. There are clearly other options, like renegotiating with the bondholders or refinancing the debt, which would leave the ownership of the jail with the County and may be more attractive. They might, however, force the County to re-categorize the debt as something other than lease-revenue bonds, which might be embarrassing. But that should not dictate the solution.

Comments

Join the Discussion on Facebook

Join the discussion on Facebook.